When you start accepting card payments online or in person, you quickly run into two terms that sound similar but mean very different things: payment gateway vs merchant account. Understanding the difference isn’t just technical trivia. It affects your approval rates, fees, cash flow, and how easily you can scale or switch providers in the future.

In this guide, we’ll break down payment gateway vs merchant account in plain language, explain how they work together, compare all the key differences, and give you practical guidance on which setup is right for your business now and in the future.

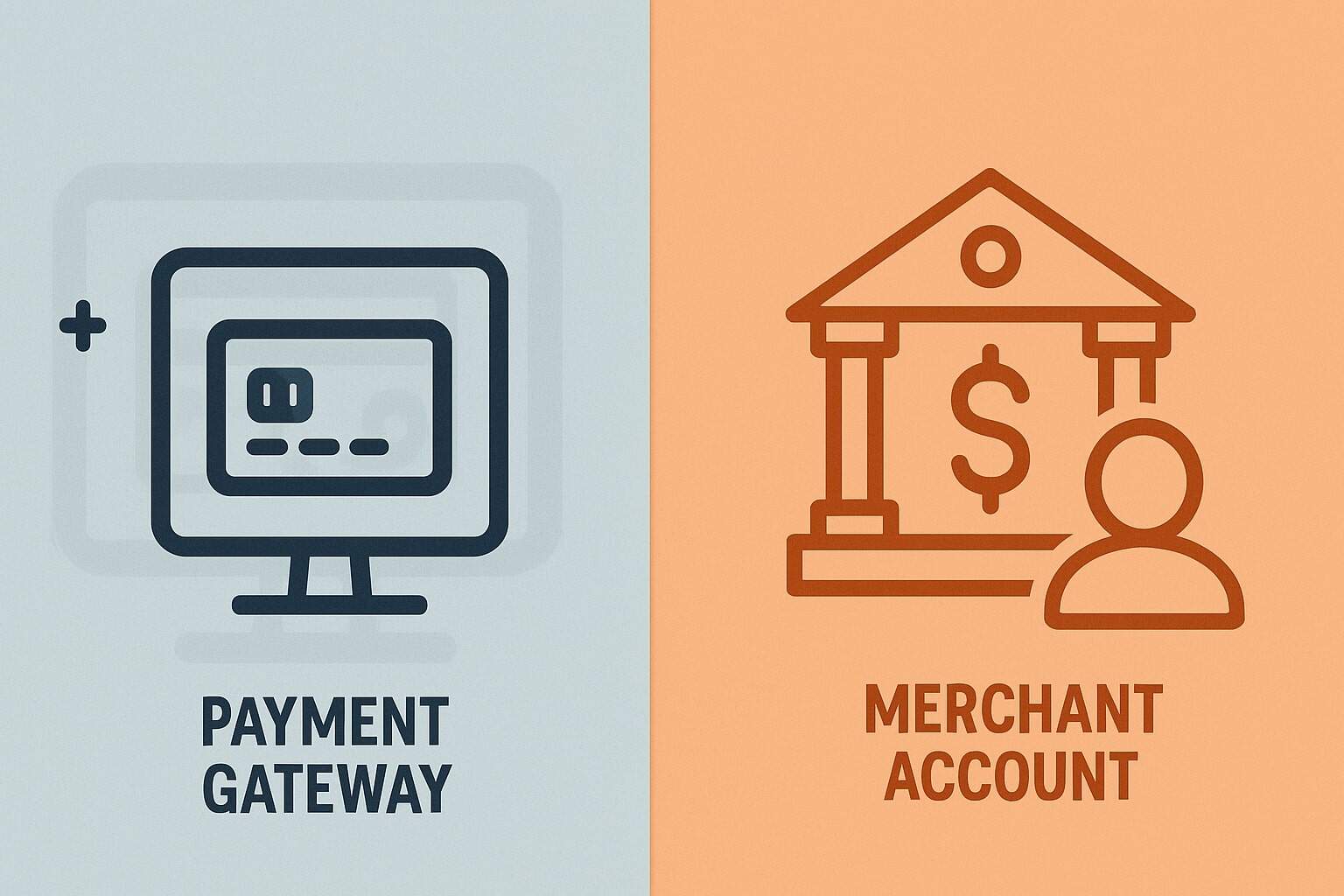

What Is a Payment Gateway?

A payment gateway is the technology that securely transmits payment data from your customer to the payment processor and back again with an approval or decline message. When people compare payment gateway vs merchant account, the gateway is the front-end piece that your customer touches.

Think of a gateway as a secure digital card terminal embedded into your website, mobile app, or point-of-sale system. When a customer enters card details or uses a stored payment method, the gateway encrypts that data, sends it through the card networks for authorization, and returns the result in a few seconds.

A modern payment gateway typically provides:

- Hosted payment pages and checkouts

- API and SDKs for custom integrations

- Tokenization, so your systems don’t store raw card numbers

- Fraud tools like address verification (AVS), CVV checks, device fingerprinting, and velocity rules

- Recurring billing and subscriptions

- Support for digital wallets like Apple Pay, Google Pay, and PayPal

- 3D Secure / Strong Customer Authentication support for extra verification where needed

The gateway does not hold your money. That’s where the merchant account comes in. The gateway simply passes transactions along to be authorized and later settled into your bank account via the acquiring side.

Because of this, when you analyze payment gateway vs merchant account, remember: the gateway is about data and approvals, not funds and deposits. It’s the bridge that connects your checkout, your customers’ cards, and the rest of the payment ecosystem.

How a Payment Gateway Works Step by Step

To truly understand payment gateway vs merchant account, it helps to see where the gateway fits into the payment flow. Here’s what typically happens when a customer pays on your site:

- Customer initiates payment: They enter card details (or use a stored token) on your checkout page, which is connected to your payment gateway.

- Encryption and tokenization: The gateway encrypts sensitive card data and may immediately tokenize it. Tokenization replaces raw card data with a secure token that you can use for future transactions without exposing the actual card number.

- Routing to payment processor / acquirer: The gateway sends the transaction request to the payment processor or acquiring bank associated with your merchant account. This is a key link in the payment gateway vs merchant account relationship.

- Card network and issuing bank: The acquirer routes the transaction through the card network (Visa, Mastercard, etc.) to the cardholder’s issuing bank, which checks whether the transaction should be approved.

- Authorization response: The issuing bank returns an approval or decline code. The network passes that response back to the acquirer, then the gateway, and finally your website or app.

- Real-time customer feedback: The gateway updates your checkout to show success or failure, often within seconds. It may also trigger webhooks or notifications to your back-end systems.

- Settlement and funding: Later (usually at the end of the day), approved authorizations are “captured” and batched for settlement. This is handled by your merchant account and processor, not by the gateway itself.

Modern gateways also add value through advanced tools like machine-learning fraud detection, card account updater services, and support for multiple currencies and local payment methods. As online commerce evolves, the gateway is becoming a central orchestration layer that helps optimize routing, reduce fraud, and improve conversion.

What Is a Merchant Account?

If the payment gateway is your messenger, a merchant account is your business’s payment “holding tank” where card funds are routed before being transferred to your regular bank account. When comparing payment gateway vs merchant account, the merchant account is the financial piece of the puzzle.

A merchant account is a special type of account provided by an acquiring bank or a payment processor. It’s not the same as your everyday business checking account. Instead, it sits in between the card networks and your bank account to:

- Receive and hold funds temporarily after settlements

- Handle chargebacks, refunds, and fees

- Ensure compliance with card network rules

- Manage risk exposure for the acquirer

When you sign up for a merchant account, your business goes through an underwriting process. The provider looks at your industry, chargeback risk, financial health, and processing history.

This underwriting step is one of the clearest distinctions in the payment gateway vs merchant account discussion: gateways focus on secure transmission, while merchant accounts focus on risk and settlement.

A merchant account typically includes:

- An account ID / MID used to route your transactions

- A defined fee structure (interchange plus or flat rate)

- Funding schedule (e.g., next-day or 2–3 business days)

- Policies for chargebacks and disputes

- Limits for monthly processing volume or ticket size

Without a merchant account (or a provider that offers a pooled account model), you can’t actually receive card payments. The merchant account is what connects your transactions to real deposits.

How a Merchant Account Works in Practice

To understand payment gateway vs merchant account from an operational standpoint, let’s look at the merchant account’s role after the initial authorization.

- Authorization happens via the gateway: The transaction is approved and authorized for a certain amount on the cardholder’s account.

- Capture and batching: Your system (or your payment gateway) submits captured transactions in a batch to your merchant account provider. This is when you confirm you actually want to collect the authorized funds.

- Clearing and settlement: The acquirer sends the batch through the card networks for clearing. The networks move funds between issuing and acquiring banks based on interchange and scheme fees.

- Deposits (funding): After netting out fees and any reserves, your merchant account provider initiates a deposit into your regular business bank account. This typically happens on a set funding schedule.

- Chargebacks and disputes: If a cardholder disputes a transaction, the chargeback process also runs through your merchant account. Funds may be debited back out while the dispute is investigated.

- Reporting and reconciliation: Your merchant account provider gives you settlement reports, batch reports, and chargeback summaries. This financial reporting is separate from the more technical reporting offered by a payment gateway.

Future trends in merchant accounts include faster settlement (including real-time or same-day payouts) and tighter integration with instant payment rails. But regardless of these innovations, the core role of the merchant account in the payment gateway vs merchant account structure—holding and distributing funds—remains central.

Payment Gateway vs Merchant Account: Key Differences

Although they work together, payment gateway vs merchant accounts represent fundamentally different functions in the payment ecosystem. Understanding the differences will help you avoid confusion when choosing providers or evaluating all-in-one platforms.

Functional Role

- Payment gateway:

- Handles data transmission, encryption, and customer-facing checkout.

- Provides integration tools like APIs, plugins, and hosted forms.

- Offers fraud tools, tokenization, and sometimes routing optimization.

- Handles data transmission, encryption, and customer-facing checkout.

- Merchant account:

- Handles funds, settlement, and deposits.

- Manages risk, underwriting, and chargeback exposure.

- Sets your pricing structure and funding schedules.

- Handles funds, settlement, and deposits.

In other words, when comparing payment gateway vs merchant account, the gateway is about secure communication, while the merchant account is about financial settlement and risk.

Ownership and Setup

- Payment gateway:

- Often quick to set up; in some cases, you can start sandbox testing in minutes.

- May not require a full underwriting process for test mode or trial access.

- You can use a standalone gateway with many different merchant accounts in more advanced setups.

- Often quick to set up; in some cases, you can start sandbox testing in minutes.

- Merchant account:

- Requires application and underwriting.

- Approval depends on your industry, credit, processing history, and risk profile.

- High-risk businesses may see stricter terms, higher fees, or rolling reserves.

- Requires application and underwriting.

Fees and Pricing

Another critical dimension of payment gateway vs merchant account is the fee structure.

- Payment gateway fees may include:

- Per-transaction gateway fee

- Monthly gateway or platform fee

- Fees for value-added services (fraud tools, recurring billing, tokenization at scale, etc.)

- Per-transaction gateway fee

- Merchant account fees may include:

- Interchange and network assessment fees

- Processor markup (percentage and/or per-transaction)

- Monthly minimums

- Chargeback and retrieval fees

- PCI compliance fees

- Interchange and network assessment fees

In many modern “all-in-one” providers, gateway and merchant account fees are combined into a single per-transaction rate. However, the underlying distinction between payment gateway vs merchant account still exists—even if it’s hidden behind a unified interface.

Technical vs Financial Risk

- Gateway risk:

- Focuses on data security and uptime.

- If the gateway goes down, you can’t accept transactions, but already settled funds remain safe with the acquirer.

- Focuses on data security and uptime.

- Merchant account risk:

- Focuses on financial exposure, fraud, and chargebacks.

- Providers may hold reserves, terminate accounts, or adjust terms if risk increases.

- Focuses on financial exposure, fraud, and chargebacks.

When you evaluate payment gateway vs merchant account, think about where your biggest vulnerabilities lie—technical (integration, uptime, checkout UX) or financial (chargebacks, reserves, cash flow). You need both sides managed well for a healthy payment setup.

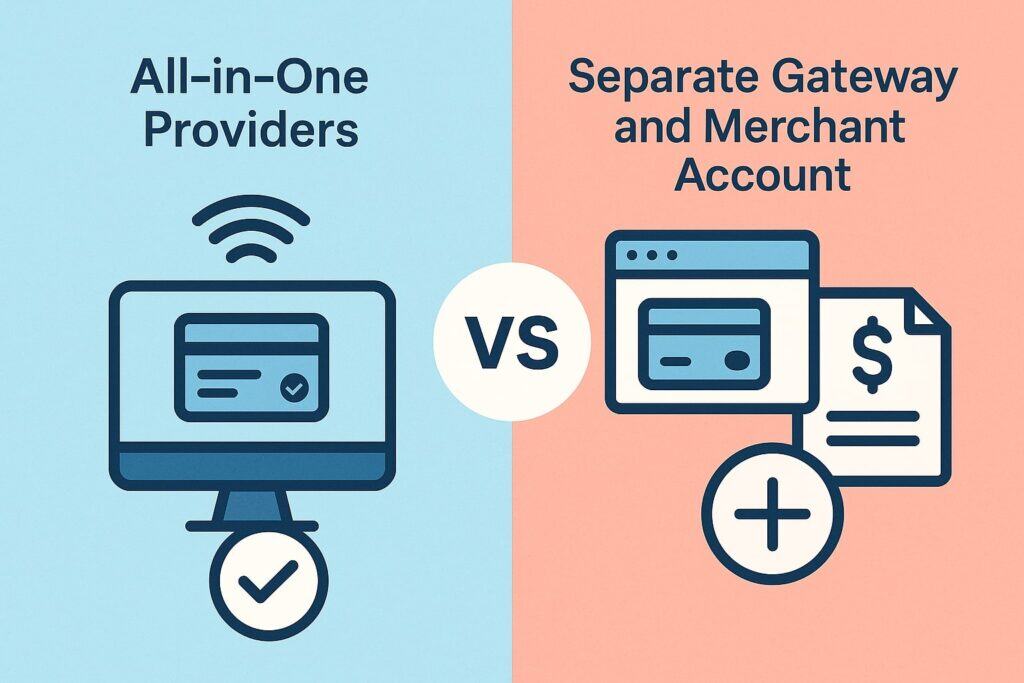

All-in-One Providers vs Separate Gateway and Merchant Account

A big reason payment gateway vs merchant account is confusing is that many modern providers bundle both into one solution. Stripe, Square, and similar platforms act as both payment gateway and merchant account (often via pooled or aggregated merchant models).

All-in-One (Integrated) Solutions

With an all-in-one platform:

- You sign up once and get both the payment gateway and merchant account services.

- You usually get a simple, flat-rate pricing structure that hides the underlying interchange and markup.

- Integration tends to be easier, with a single API and dashboard.

- Payouts, disputes, and reporting are all managed in one place.

For many smaller or growing businesses, an integrated provider simplifies the entire payment gateway vs merchant account decision. You don’t have to manage separate vendors, and you get to market faster.

Separate Gateway + Merchant Account

Larger or more complex businesses often prefer a separate gateway and merchant account setup:

- You can negotiate interchange-plus pricing directly with an acquirer for better rates.

- You can use a multi-acquirer strategy, routing transactions through multiple merchant accounts for redundancy or cost optimization.

- You can keep your gateway integration consistent while switching acquirers or adding local acquiring in new regions.

The trade-off is complexity. Managing separate contracts, integrations, and reporting systems takes more effort. But if you have the volume and experience, separating the payment gateway vs merchant account can unlock better economics and more control.

Pros and Cons of Each Approach

When debating payment gateway vs merchant account and whether to bundle or separate them, weigh these trade-offs:

All-in-one (Gateway + Merchant Account):

- Pros:

- Fast time to market

- Simple pricing and contracts

- Unified dashboard and support

- Good developer experience

- Fast time to market

- Cons:

- Less control over interchange and markup

- Harder to switch providers later

- May not offer advanced routing or custom risk settings

- Aggregated merchant model can mean stricter account holds for certain risk profiles

- Less control over interchange and markup

Separate Gateway and Merchant Account:

- Pros:

- Potentially lower processing costs at scale

- Flexibility to swap acquirers or add redundancy

- Advanced control over routing and risk

- Clearer distinction in responsibilities between partners

- Potentially lower processing costs at scale

- Cons:

- More complex setup and integration

- Multiple contracts, support contacts, and dashboards

- Requires more in-house payments expertise

- More complex setup and integration

Ultimately, the right structure for payment gateway vs merchant account depends on your size, risk profile, growth plans, and internal resources.

How to Choose Between Payment Gateway vs Merchant Account Options

Choosing between different payment gateway vs merchant account setups starts with your business model, not the technology. Ask yourself a few key questions:

1. What Channels and Payment Methods Do You Need?

- Are you online-only, in-person, or omnichannel?

- Do you need eCommerce, invoicing, recurring billing, or all of the above?

- Which methods matter most—credit and debit cards, ACH, digital wallets, buy now pay later (BNPL)?

Your answers drive which gateways you should consider and whether you need a merchant account that supports card-present and card-not-present transactions together.

2. What Is Your Risk Profile?

- High-risk industries (e.g., certain subscription models, travel, adult, CBD, firearms) often face stricter underwriting.

- Chargeback-prone categories need strong dispute management and fraud tools baked into both the gateway and the merchant account.

When comparing payment gateway vs merchant account, make sure both sides are comfortable with your industry. A mismatch can lead to sudden account closures or funding holds.

3. How Important Is Pricing Optimization?

If you’re small or early-stage, a flat-rate, all-in-one provider may be ideal. The trade-off between ease and cost is usually worth it.

As your processing volume grows, it may become cheaper to:

- Negotiate interchange-plus pricing with a merchant account provider.

- Use a gateway that supports smart routing, so you can send transactions to different acquirers based on card type, region, or risk.

In that phase, the structure of payment gateway vs merchant account becomes more strategic.

4. How Much Technical Control Do You Want?

Developers often care deeply about:

- API quality and documentation

- Webhooks and event streams

- Sandbox environments and test cards

- Ability to customize the checkout experience

If developer experience is mission-critical, you might start with a gateway-first mindset and then choose a merchant account provider that integrates cleanly with that gateway. That’s another way to think about payment gateway vs merchant account: lead with the technology partner or the financial partner, depending on your priorities.

Security, Compliance, and Risk Management

Security and compliance are essential in the payment gateway vs merchant account comparison because both components must protect cardholder data and follow industry rules.

Gateway Responsibilities

A payment gateway typically:

- Provides PCI DSS–compliant methods to collect card data (hosted fields, iFrames, or redirect pages).

- Encrypts data in transit and often in storage (when tokenizing).

- Offers tools like 3D Secure, device fingerprinting, and rules-based fraud filters.

Good gateways help reduce your PCI scope by keeping raw card data out of your servers. This significantly lowers your compliance burden and risk.

Merchant Account Responsibilities

A merchant account provider focuses on:

- Monitoring fraud and chargeback ratios.

- Applying velocity controls and other risk rules at the processor level.

- Managing chargeback workflows, notifications, and representments.

- Ensuring compliance with card brand rules and regulations.

Because both sides matter, a strong payment gateway vs merchant account strategy involves picking partners that collaborate well on security and fraud. For example, your gateway might flag suspicious behavior, while your acquirer sets rules about when to auto-block transactions.

As regulations evolve and card networks push for stronger authentication and data protection, both the gateway and the merchant account will likely see more built-in tools and requirements. Future improvements may include more AI-driven risk scoring and automated dispute handling.

Future Trends Affecting Payment Gateway vs Merchant Account

The distinction between payment gateway vs merchant account is not going away, but how these services are delivered is evolving rapidly.

Embedded Payments and Platforms

More software platforms (like SaaS tools and marketplaces) are embedding payments directly into their products. Under the hood, they still rely on payment gateway vs merchant account components, but these are abstracted away behind a platform interface.

If you run a platform, you might:

- Use an API-first gateway that lets you manage sub-merchants or connected accounts.

- Work with a merchant account provider that supports platform and marketplace models.

As this trend grows, businesses will focus less on raw payment gateway vs merchant account choices and more on which platforms best support their entire lifecycle.

Real-Time Payments and Alternative Rails

Instant payment networks and alternative rails (like RTP or FedNow for bank transfers) are shifting how money moves. Over time, this may change:

- How merchant accounts handle funding speed and payout options.

- How gateways support multiple payment rails beyond cards and ACH.

However, even with faster bank payments, cards will remain a major channel. So the core payment gateway vs merchant account structure is likely to stay, with additional modules for real-time and account-to-account payments layered on top.

AI-Driven Fraud and Optimization

Artificial intelligence and machine learning are increasingly used in both gateways and merchant accounts to:

- Predict fraud in real time

- Optimize authorization rates

- Route transactions dynamically based on issuer behavior and cost

In future setups, your payment gateway vs merchant account combination might include:

- A gateway that sends enriched data and risk scores with each transaction

- An acquirer that applies advanced authentication and routing logic based on that data

Choosing partners with strong AI-driven features can improve approvals and reduce fraud, directly impacting your revenue.

FAQs

Q.1: Do I Need Both a Payment Gateway and a Merchant Account?

Answer: In most card-not-present scenarios, yes. You need a payment gateway vs merchant account combination to handle both the technical and financial sides of payment processing. However:

- If you choose an all-in-one provider, they supply both components under one contract.

- If you go the traditional route, you choose a standalone gateway and pair it with a separate merchant account.

The underlying functions are always there—you just decide whether to bundle them or manage them separately.

Q.2: Is a Payment Service Provider the Same as a Merchant Account?

Answer: A payment service provider (PSP) often acts like a hybrid of payment gateway vs merchant account. Many PSPs:

- Provide a gateway for transaction processing.

- Use an aggregated merchant account model, where multiple merchants share one master account.

In that setup, you technically don’t have your own dedicated merchant account ID. Instead, the PSP manages the pooled merchant relationship with the acquirer, and you operate as a sub-merchant. This can simplify onboarding but sometimes means more conservative risk controls.

Q.3: Can I Switch Merchant Accounts Without Changing My Payment Gateway?

Answer: In many cases, yes. One advantage of keeping payment gateway vs merchant account separate is that you can:

- Maintain your existing gateway integration and customer experience.

- Add or switch merchant account providers on the back end.

This flexibility allows you to negotiate better rates, add local acquirers for international expansion, or build redundancy. However, not all gateways support this multi-acquirer approach, so verify capabilities before committing.

Q.4: How Do Fees Work in Payment Gateway vs Merchant Account Models?

Answer: Fees depend heavily on your provider and pricing model. Common elements include:

- Gateway fees: per-transaction fee, monthly fee, add-ons for fraud tools and subscriptions.

- Merchant account fees: interchange, assessments, markup, chargeback fees, PCI fees, monthly minimums.

All-in-one providers blend payment gateway vs merchant account fees into a simple rate like “2.9% + $0.30 per transaction.” Traditional setups separate each component. As your volume grows, understanding these pieces helps you negotiate smarter.

Q.5: Which Is More Important: Payment Gateway or Merchant Account?

Answer: Neither side is more important; both are essential. The payment gateway vs merchant account distinction is about different roles, not hierarchy:

- A poor gateway can cause declined transactions, slow checkout, or integrations that constantly break.

- A poor merchant account can lead to high fees, funding delays, and surprise reserves or terminations.

Aim for a balanced solution where both the gateway and merchant account match your business needs, technical stack, and risk profile.

Conclusion

Understanding payment gateway vs merchant account is a foundational step in designing a payment stack that supports your growth. The gateway handles secure data transmission, customer experience, and technical integrations. The merchant account handles settlement, pricing, and risk.

You can choose:

- An all-in-one provider that bundles payment gateway vs merchant account into a single, simple solution, ideal for getting started quickly.

- A more advanced setup where you select a best-in-class gateway and pair it with one or more merchant accounts to optimize cost, redundancy, and control.

As payment technology continues to evolve—with embedded payments, real-time rails, and AI-driven fraud tools—the line between payment gateway vs merchant account may feel more abstract. But behind the scenes, you’ll always need both functions: one to move data securely, the other to move money reliably.

If you treat your payment stack as a strategic asset, not just a cost center, the way you choose and manage your payment gateway vs merchant account can boost approvals, reduce risk, and improve your customers’ checkout experience—today and in the future.