By Thomas Brandt March 13, 2026

SaaS platforms and marketplaces increasingly integrate payments into their products. Whether it’s enabling creators to receive subscription payments, contractors to send invoices, or sellers to receive checkout payments, the underlying processing model will have significant implications for revenues, compliance, and risks.

Many founders focus on speed to market while ignoring the underlying structural differences in becoming a Payment Facilitator (PayFac), using an Independent Sales Organization (ISO), or using a Payment Service Provider (PSP).

These models define who performs underwriting, who assumes fraud risk, and how revenues are split, among other factors. Making the wrong choice can limit a company’s potential or increase compliance risks. Knowing the differences helps platforms better align their payment strategy with their operational maturity and scalability aspirations.

Table of Contents

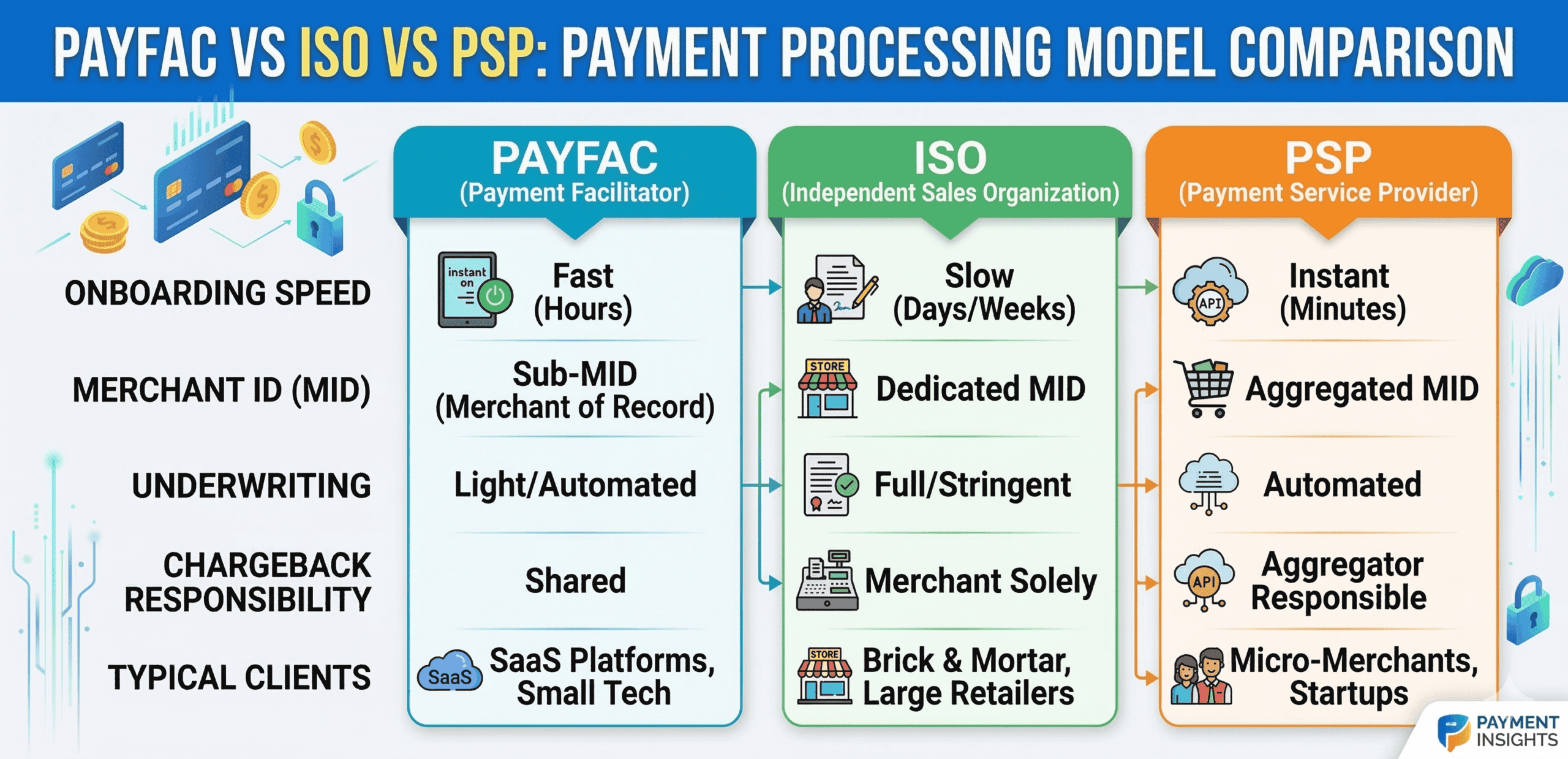

What a Payment Facilitator Really Is

Payment Facilitator, on the other hand, works as a master merchant and facilitates the onboarding of sub-merchants under its umbrella. Instead of each merchant requiring its own merchant account, the PayFac sponsors them under a single relationship with an acquiring bank.

This model provides great benefits to SaaS and marketplace businesses in terms of control and monetization. However, it also adds a layer of risk and complexity. The PayFac model requires the Payment Facilitator to underwrite, monitor, and conduct KYC and fraud risk assessments for each sub-merchant.

Understanding the ISO Model

An Independent Sales Organization is an intermediary between merchants and acquiring banks. ISOs usually refer to onboard merchants with a sponsoring bank. However, they do not refer to merchants under a master account.

For a SaaS company, working with an ISO is beneficial because compliance requirements are relatively low compared to those of a PayFac. The acquiring bank still handles the underwriting. The sponsoring banks also handles risk management and regulatory requirements.

However, the level of customization is low with the ISO model. The flow is not fully under the company’s control. Additionally, revenue streams may be limited. The ISO approach suits businesses that want to be involved in payments without assuming full ownership of compliance.

What a PSP Brings to the Table

A Payment Service Provider (PSP) provides a plug-and-play payment solution. Merchants are usually onboarded as a group under the PSP umbrella, and underwriting, compliance, and risk management are handled by the PSP.

PSPs provide a fast and easy solution for SaaS platforms. Integration is fast through APIs, and onboarding is easy. Fraud management and monitoring tools are usually integrated.

The drawback of a PSP is that it compromises control. Pricing models are usually fixed, and flexibility is limited in some cases. The PSP also prevents the platform from fully owning the brand. The PSP model is good for early-stage companies that want to focus on speed to market and minimize compliance costs.

Underwriting Responsibility Differences

“Underwriting responsibility” is the term used to describe risk ownership. When you use a PayFac model, your platform underwrites the sub-merchant directly. This means you verify the sub-merchant identity, evaluate the business model, check for illicit activities, and determine the level of risk.

When you use an ISO model, underwriting is usually handled by the sponsoring bank; however, the platform may help gather documents. When you use a PSP model, the underwriting is primarily done by the PSP.

While the more underwriting you do, the more revenue you can share, the more you also risk if the merchant is fraudulent or excessively charged back. Underwriting is not just paperwork; it is a financial gatekeeping function.

KYC and Regulatory Exposure

Know Your Customer requirements escalate from PSP, to ISO, and then to PayFac. For PayFacs, identity verification, sanctions checking, and ongoing monitoring are necessary.

For ISOs, regulatory oversight exists, but the sponsor’s bank has a say. For PSPs, centralizing regulatory requirements significantly reduces the regulatory burden on the business.

It’s common for founders to underestimate the business operations implications of Know Your Customer requirements. Regulatory maturity needs to be commensurate with the chosen business model.

Fraud Monitoring and Risk Controls

The level of fraud risk increases with the level of control. A PayFac must monitor the entire portfolio of sub-merchants for suspicious patterns. Too much fraud or chargeback activity can put the master account at risk.

ISOs are aware of the risk level with the acquiring bank, but they don’t bear the primary portfolio’s risk. PSPs generally bear the risk level for monitoring the merchants for fraud, utilizing a centralized system to manage the risk for thousands of merchants.

If you choose the PayFac route, transaction monitoring tools, dispute management tools, and analysis infrastructure become critical.

Revenue Potential and Economics

The highest potential for revenue upside is offered by the PayFac model, which allows for participation in the economics of transactions, such as a share of the fees for processing transactions. The ISO model usually provides a referral fee or a share of the revenue, but the margins are lower.

The PSP model provides a fixed revenue-sharing model, which is relatively inflexible. While the PayFac model has attractive economics, they need to support the cost of compliance. The revenue opportunity should match the expected volume of transactions.

Onboarding and User Experience

Embedded onboarding plays a role in the rate of seller onboarding. PayFac structures enable the platform to design seamless onboarding within the product interface.

ISO relationships may involve additional bank-related steps. PSPs provide a digital onboarding process, with some brand elements still external. If user experience is a key aspect of your platform’s value proposition, then onboarding friction is an issue. However, it must never sacrifice compliance verification.

Scaling Operational Complexity

However, with the increase in transaction volume, the complexity of the operations also rises. For the PayFacs model, the concept of scaling is not only about handling more transactions; it is also about continually monitoring the portfolios, updating the underwriting levels, and handling chargebacks.

Compliance checks, merchant re-verification, and fraud analysis also need to be scaled with the revenue. However, if the complexities are not considered, they pose a threat to the master account. ISOs scale differently. For them, the concept is more about managing the relationships and working with the sponsor banks rather than developing a complete compliance infrastructure.

PSPs help the payment platforms scale by centralizing the concept of scaling. This way, the payment platforms can grow without requiring a significant increase in the internal staff. For any payment platform, the concept of scaling requires an honest assessment of the infrastructure. Expansions need to be considered based on operational readiness rather than revenue readiness.

When PSP Simplicity Wins

For early-stage startups, simplicity can be more important than control. PSP integration can save significant time and reduce regulatory barriers for startup launches. Startups can avoid developing their own underwriting, monitoring, and audit documentation. Instead, they can leverage the infrastructure provided by the PSP.

If you compete on software features, not payment economics, simplicity can help. Revenue participation might not be significant, but risk is still controlled. Simplicity of PSPs works best when the payment business is an enabler, not a definer. Control makes sense when transaction volume and human resource maturity justify taking on deeper financial and regulatory responsibility.

When the PayFac Model Is Strategic

This PayFac approach becomes a strategic option if the payment volume is considerable and the monetization opportunity is substantial. Companies with well-developed compliance, underwriting, and fraud detection systems have an easier time dealing with the complexity. Controlling the onboarding process, pricing structures, and products helps in building loyalty with the ecosystem.

But infrastructure comes before aspiration. For this to work, risk management tools, disputes, and audits are essential. Without this, the compliance burden may outweigh the financial benefits.

PayFac changes the nature of a SaaS company to a financial intermediary with regulatory risk. When operational disciplines align with scale, this approach provides great benefits. Without this, it adds unnecessary risk and financial instability.

Conclusion

The decision to go with a PayFac model, ISO model, or PSP model is not merely a technological one; rather, it is a strategic one that impacts compliance risk, revenue model, and operational responsibility. PSPs give speed and lower regulatory hurdles, making them perfect for young platforms that are focused on growth.

ISOs give balanced participation with moderated oversight. PayFac gives maximum control and monetization opportunities but demands mature underwriting, fraud management, and governance. Each model has trade-offs between flexibility and responsibility.

For SaaS platforms and marketplaces, it is important to consider their own resources and long-term plans before making a decision. If the payment structure matches their operational maturity, they can scale their business without compromising compliance, merchant trust, or financial integrity in the long run.

FAQs

What is the greatest risk associated with joining PayFac?

Taking up underwriting and fraud responsibilities for every submerchant under your umbrella account is the main risk.

Is a PSP the safest option in every situation?

PSPs lessen the overhead of compliance, but they severely restrict monetization flexibility and pricing control.

What distinguishes ISO from PayFac?

A PayFac unifies sub-merchants under a master account, whereas an ISO processes transactions for merchants separately.

Can platforms switch models later?

Yes, but migration requires careful planning, regulatory review, and merchant communication to avoid disruption.

Which model generates the most revenue?

PayFac typically offers the highest revenue potential, but only when operational maturity supports increased risk exposure.